Oscar Health: A 2026 Rebound (Ticker: OSCR)

Short-term speed bumps in the health insurance market are giving us a buying opportunity

“The number one is, did we and our competitors price market morbidity correctly? Because when I look at my peers and I see pricing where we’re all kind of in the same band, it’s not like there’s a whole bunch of people that have taken different points of view as to what morbidity is going to be next year. That might be because a whole bunch of consultants were walking around selling their information to all of us over and over again. And we all took input from similar sources. I would, first of all, say that if you believe that we’re mispriced, I think you probably think the market’s mispriced. The biggest risk for this industry is going to be, what’s the market morbidity next year? We believe that we built in more than enough for us to accommodate that in our pricing.” - CFO Scott Blakely, UBS Global Healthcare Conference, November 2025

Health insurers such as Oscar Health (ticker: OSCR) have been caught off guard in 2025 with rising healthcare utilization. This, in turn, has caused Medical Loss Ratios (MLR, or the % of claims paid out vs. premiums earned in a given period) to be abnormally high.

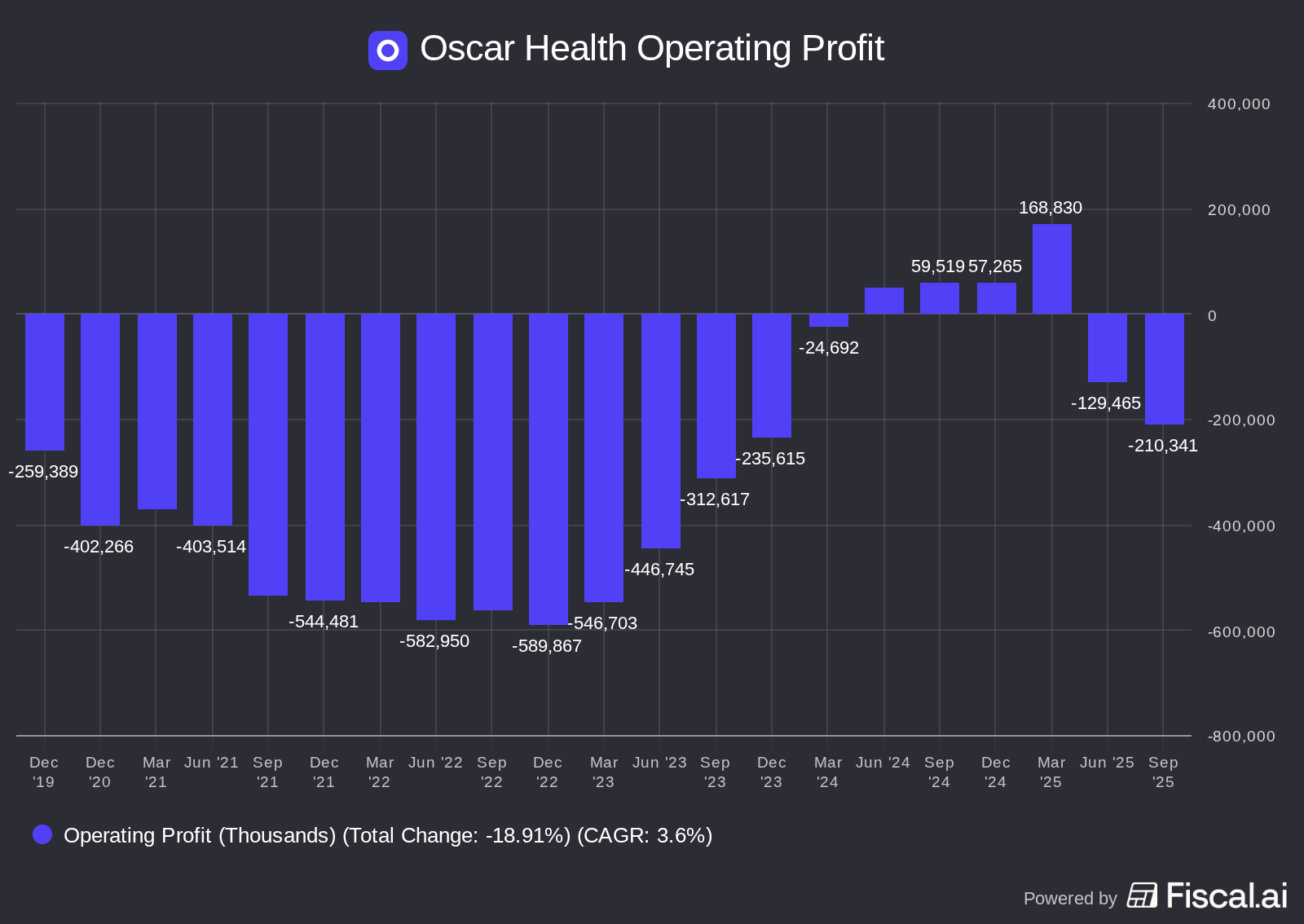

For an upstart with less scale than the legacy players, a rising MLR has reversed Oscar Health’s operating leverage, sending it from a LTM operating profit of $168 million in March 2025 to a $210 million loss in September. 2025 guidance calls for a $250 million loss at the midpoint.

My thesis is simple: 2025 is a temporary blip for Oscar Health’s MLR. Over the next decade, it has a clear path to MLR stability, improved operating leverage, and market share gains, which should provide the stock with upside in 2026 and the potential for ten-bagger returns over the next decade.

In this update, I will discuss:

Q3 earnings, 2026 pricing, and ACA market uncertainty

The importance of the SG&A ratio

What will cause the stock to get “unstuck”

Whether Oscar Health still has an emerging moat

Anyone can read my complimentary introductory research report on Oscar Health, which was published in July 2025.

Here is the Q1 schedule for Emerging Moats Research. Full reports will be coming out on Evolus, MercadoLibre, and Nelnet. Reach out to get your (one-time) complimentary trial to check out the service.

Subscribe to Emerging Moats here:

2026 Pricing and ACA Subsidies

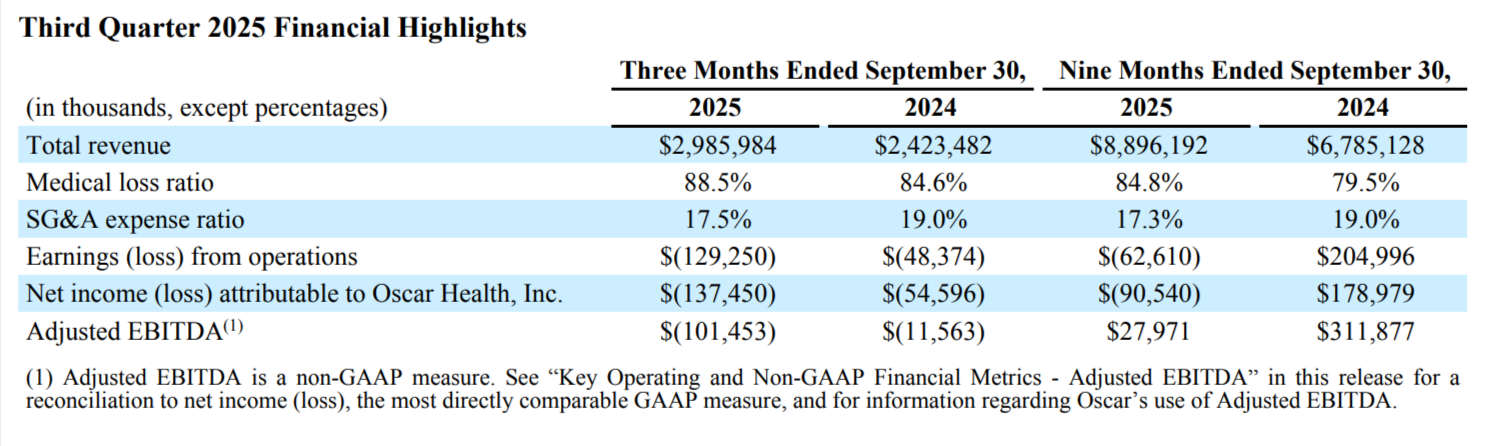

Oscar Health’s Q3 earnings were in line with expectations, albeit low ones. Beginning in the spring of 2025, insurance claims exceeded previous estimates, resulting in an increase in the MLR. Seeing as Affordable Care Act (ACA) marketplace plans are repriced annually, it is stuck with these poor metrics for the rest of 2025 if current trends persist.

Q3’s MLR was 88.5% compared to 84.6% in the same quarter a year ago. For the first nine months of 2025, the MLR was 84.8% vs. 79.5%. Quarterly MLR will trend higher throughout the year as more ACA payors reach their maximum out-of-pocket expense, meaning you have higher claims paid out vs. the same monthly premiums.

After bringing in experienced insurance executive Mark Bertolini as CEO in early 2023, Oscar Health quickly found cost discipline. In 2023 and 2024, Oscar’s MLR was slightly below 82%. Progress on overhead spending helped the company generate positive operating earnings in 2024.

In 2025, the MLR is expected to be 86% to 87%, erasing its thin operating profit.

What helps me give Bertolini and Oscar Health a pass on mispricing in 2025 is the fact that every health insurer has been blindsided by underestimating morbidity and utilization this year. United Health’s MLR is estimated to be 89%. That is its highest level since 2011. From 2011 - 2022, its MLR was never above 83%.

Regulations mandate a maximum MLR of 80% in the ACA marketplace. If Oscar Health prices its plans too high and generates an MLR below 80%, it will be forced to rebate customers for overcharging them on monthly premiums. The ideal range for an ACA insurer is an MLR in the low 80s. This allows you to price your plans competitively and generate a profit.

In 2026, Oscar Health is hiking its monthly premiums by an average of 28%. There will always be uncertainty around pricing and policy utilization in any given year. However, if you look at the historical MLRs of legacy insurers such as UnitedHealth, more often than not, the actuarial projections are accurate.

Which brings us to the ACA subsidies political football. Subsidies for ACA plans were expanded to a wider demographic in 2021. These subsidies are set to expire in 2026 unless Congress intervenes. As I write this on December 21st, it looks more likely than not that the ACA subsidies will not be renewed.

Oscar Health has priced its plans for 2026 assuming that these subsidies do not return. If they do, the company and the rest of the insurance market will likely achieve MLRs below the 80% maximum, resulting in a significant improvement in profitability in 2026. It is a heads I win (ACA subsidies get extended), tails I don’t lose (ACA subsidies go away) situation.

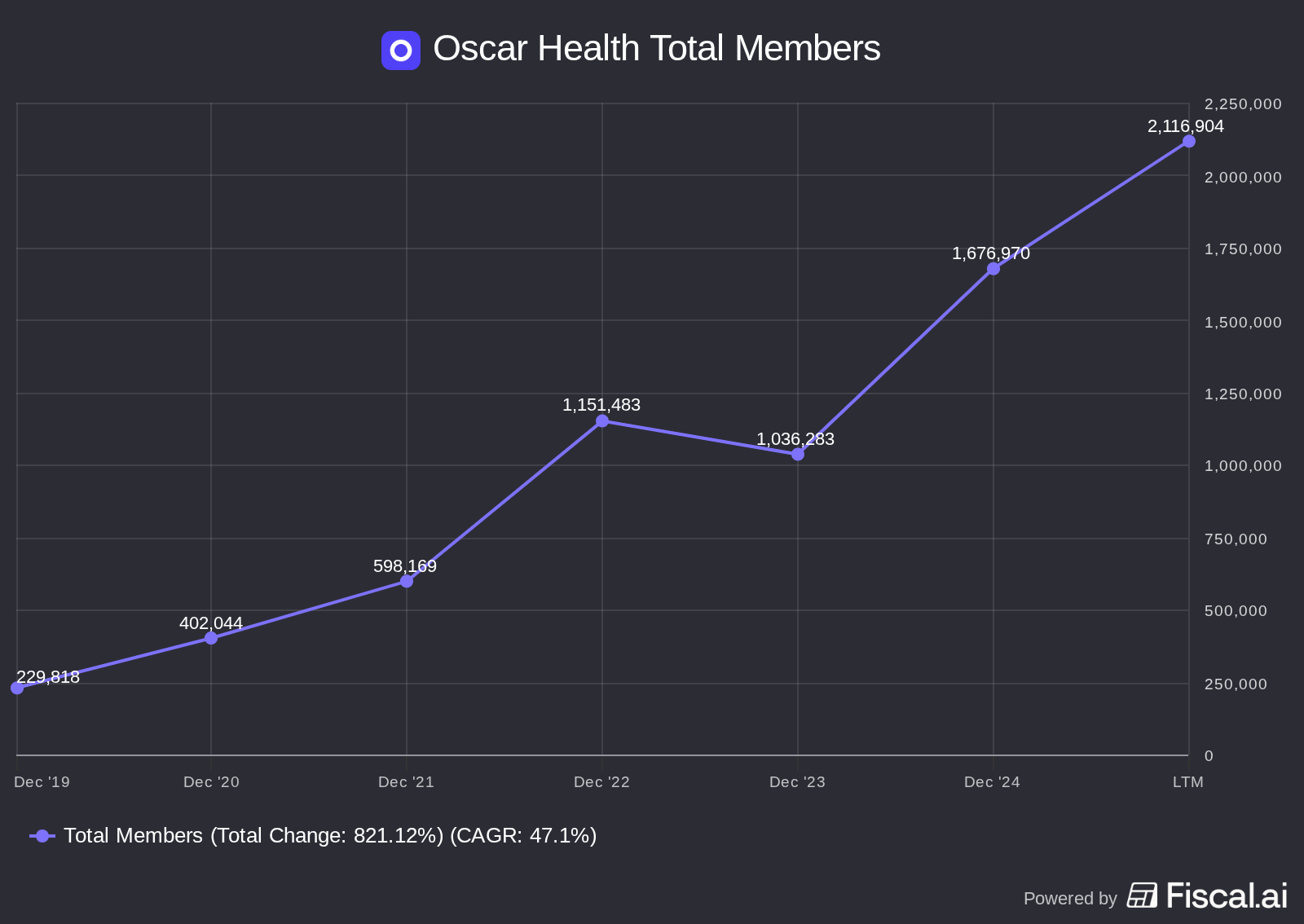

Fewer subsidies will result in fewer ACA buyers in 2026, thereby lowering Oscar Health’s addressable customer base. Total members will drop next year. By how much? That is unclear. The company will likely continue to gain market share – it entered 70 new counties during this year’s open enrollment – which will hopefully mitigate some of the customer loss.

A 28% price hike can offset many customer losses in a reset year. Even if customers decline by over 20%, Oscar Health can likely maintain its 2025 premium revenue, estimated at $12 billion to $12.2 billion, as of the latest guidance.

Over the long term, there is room for Oscar Health to continue capturing market share in the ACA and ICHRA (Individual Coverage Health Reimbursement Arrangement, where employers provide employees with funds to purchase individual plans) payor pool. Health insurance premiums in the private insurance market exceed $1 trillion. UnitedHealth alone did $339 billion in premium revenue over the last 12 months, growing at a 10% annual rate since 2012.

Even if 2026 is a speed bump for customer growth, Oscar Health has a clear path to grow its premium revenue substantially over the next decade if it can maintain its market share momentum.

Expense ratio progress

There are three factors to Oscar Health that will determine how the stock performs in 2026 and beyond. First is the MLR, which we discussed above. The other two are the SG&A ratio and maintaining its emerging moat characteristics.

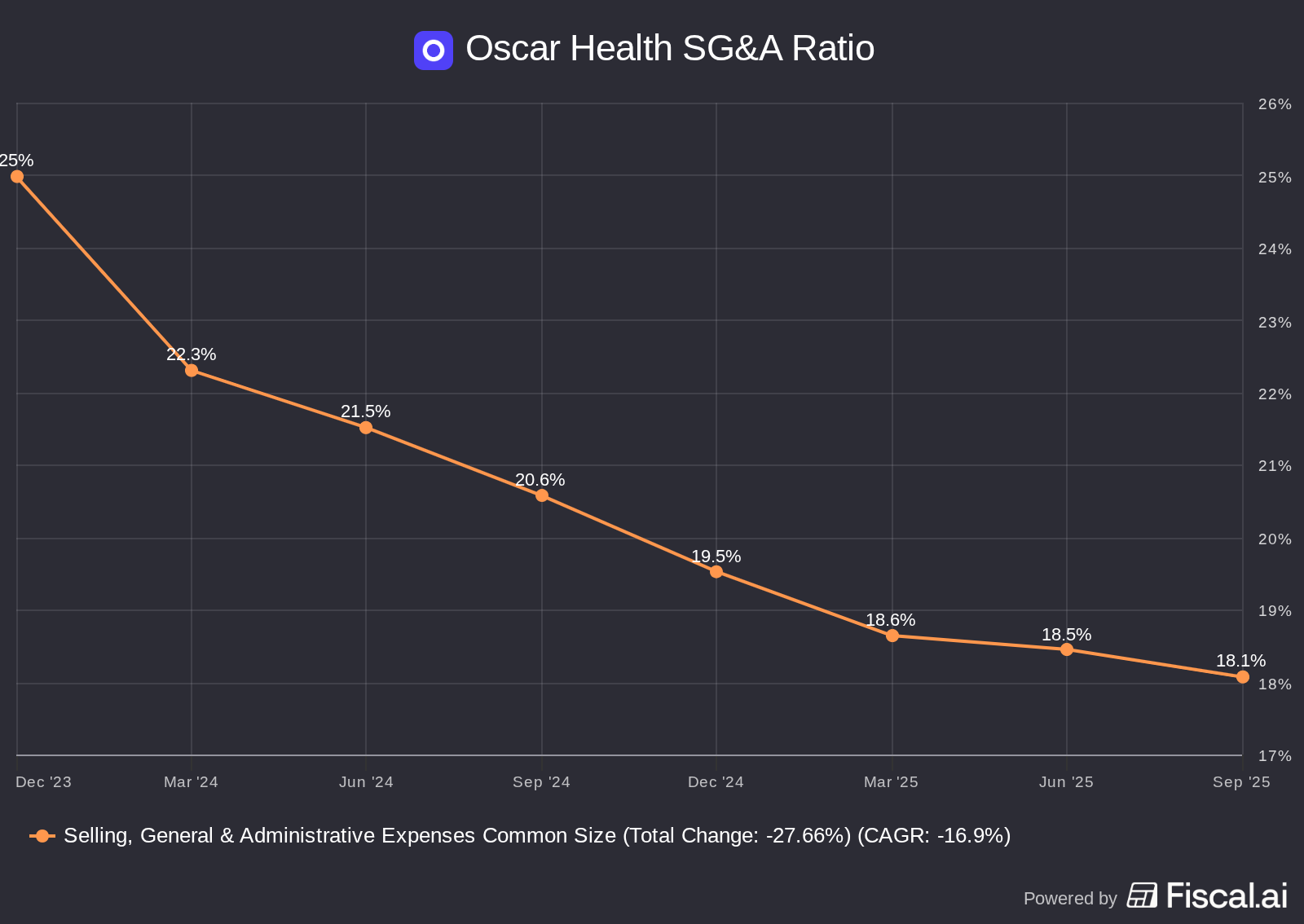

Let’s talk about the SG&A ratio. These are the overhead expenses – including executive pay, technology, and customer support – divided by total premiums earned. With a maximum MLR of 80%, the SG&A ratio is where Oscar Health can determine its own destiny when it comes to bottom-line operating margin. An SG&A ratio of 15% turns into a 5% operating margin at an 80% MLR. An SG&A ratio of 25% turns into a negative 5% operating margin. Little room for error. Scale matters.

Oscar’s claim is that its modern, technology-forward customer approach will help it attract sticky customers to its plan while also reducing overhead costs. This should materialize in a steadily declining SG&A ratio.

Since Bertolini took over, SG&A has decreased from 25% of premiums earned to 18.1% over the last twelve months and has continued to decline every quarter.

Continued investments in technology, such as automated customer support, connected healthcare communications, and a better Customer UI/UX will not only help Oscar attract more customers but also save on costs. It is already investing in building an AI agent to manage its systems, which should at least drive efficiencies on the customer support line.

At subscale premiums and with nowhere near full national coverage, Oscar Health has considerable room to improve its SG&A ratio. Legacy insurers typically have operating expense ratios of around 10%. As Oscar Health scales across its various markets, it should be able to match this SG&A ratio (if not surpass it due to its lack of tech debt).

Assuming an average MLR in the low 80s and an SG&A ratio below 15% and I think a reasonable assumption is for Oscar Health to grow into a 5% operating margin over the next five years.

Getting the stock “unstuck”

Oscar Health stock is down from its IPO and essentially flat over the last two years:

What will finally save the stock price in 2026? It will not be an ACA subsidy extension (although that would be nice). It is unlikely to be better-than-expected membership growth. It won’t be beating an EPS target. Frankly, I have no idea what Oscar Health’s EPS even is.

The key is simply proving it can hit a low 80s MLR with an improving SG&A ratio. This will demonstrate that 2025 was a blip, and the path to increasing operating leverage, which began in 2023 and continued in 2024, has resumed.

Bertolini’s spending discipline, combined with the effective utilization of modern software, will continually improve the SG&A ratio. Pricing is being taken with extreme caution across the industry to make sure the high MLRs of 2025 are not repeated. It is likely that Oscar Health’s MLR is close to 80% (or even below) in 2026. Combined with an SG&A ratio below 18%, we get a return to positive earnings.

Is there still an emerging moat? (plus, a valuation update)

In 2026, the market will focus on Oscar Health’s MLR and SG&A ratio. Over the next five years, Mr. Market will focus on (and the share price will reflect) its ability to gain market share among health insurance customers in the United States.

Market share gains will come from its emerging moat.

The initial thesis on Oscar Health’s emerging moat was twofold and remains unchanged since July.

First, Oscar Health has a larger scale compared to any technology-forward start-up in the health insurance space. A competitor starting from scratch would take years to replicate Oscar’s provider network, technology platform, and overall relationships in the ACA ecosystem. For Oscar, this meant a decade of losing money, which was lucky enough to have been funded by generous venture capital partners. I think this is a unique situation, unlikely to be replicated, which cuts off any disruptive competition from the bottom.

Second, Oscar Health is the disruptor to the legacy players. Health insurers have significant technology debt, substantial existing profit pools, and an incentive to maintain the existing system (which is often confusing and employer-focused) in order to preserve these profit pools. Oscar Health is chipping away at these moats each year with its technology-forward approach that puts the customer first. It is unlikely – if not downright impossible – for the older health insurers to combat Oscar Health’s edge.

Jesse Horowitz, VP of Member Experience, summed this up at a recent investor roundtable:

“Look, I think I’ll sound like a bit of a broken record. I think you have to stop thinking about health insurance as its own beast and think about it as any other consumer product. Oscar has been giving away free virtual urgent care since we launched our first product in 2014. That’s been a part of the offering. It’s fully integrated with the experience. It’s super convenient. As you mentioned, I use it all the time. I think it’s both a great cost-saving tool. It can be used for divergence. It could be for convenience. It kind of runs the gamut. Not everyone uses it. I see this as less about we don’t want to educate people on virtual urgent care. That is so narrow. It’s about driving awareness that there is value.

If you have a healthcare need, you open up your Oscar app, you open up your Aetna app, there are things in there that are useful. It could be a SilverSneakers program, it could be anything else. Go hire some people who are designing Airbnb and Spotify and all these highly consumer-oriented products. Have them build for healthcare and you’ll get better usability. The usability will result in people not understanding how to use these kinds of capabilities.”

Let’s talk quickly about valuation.

The stock currently has a market cap of $4 billion. Its balance sheet is well-capitalized, with $4.7 billion in cash/investments that could cover its entire benefits/risk adjustments payable of $3.33 billion, as well as $686 million in long-term debt if it were to come due tomorrow. This is unrealistic outside of the business liquidating, but it demonstrates that Oscar Health was well-prepared to deal with a down year in 2025 and is now poised to start building excess capital in 2026, with room to return cash to shareholders at some point over the next few years if management so desires.

It has just raised $410 million in convertible notes due in 2030, carrying a 2.25% interest rate and an initial conversion price of approximately $25 per share.

Convertibles and equity have been the name of the game for Oscar Health to fund its growth. LTM shares outstanding have grown at a 7.5% annual rate since 2023. Yikes. This must be taken into account in any valuation work. However, the future should see a reduced rate of dilution if the business starts generating consistent operating earnings.

So, how am I looking at the valuation? First, let’s assume that Oscar Health’s shares outstanding increase by 3% annually over the next five years, which would bring today’s market capitalization to $4.64 billion at the current share price.

In 2026, premium revenue is expected to be $12 billion. A 2% operating margin – a fair assumption if MLR normalizes and the SG&A ratio improves – would lead to $240 million in operating earnings. That is roughly 17x the current market cap of $4 billion.

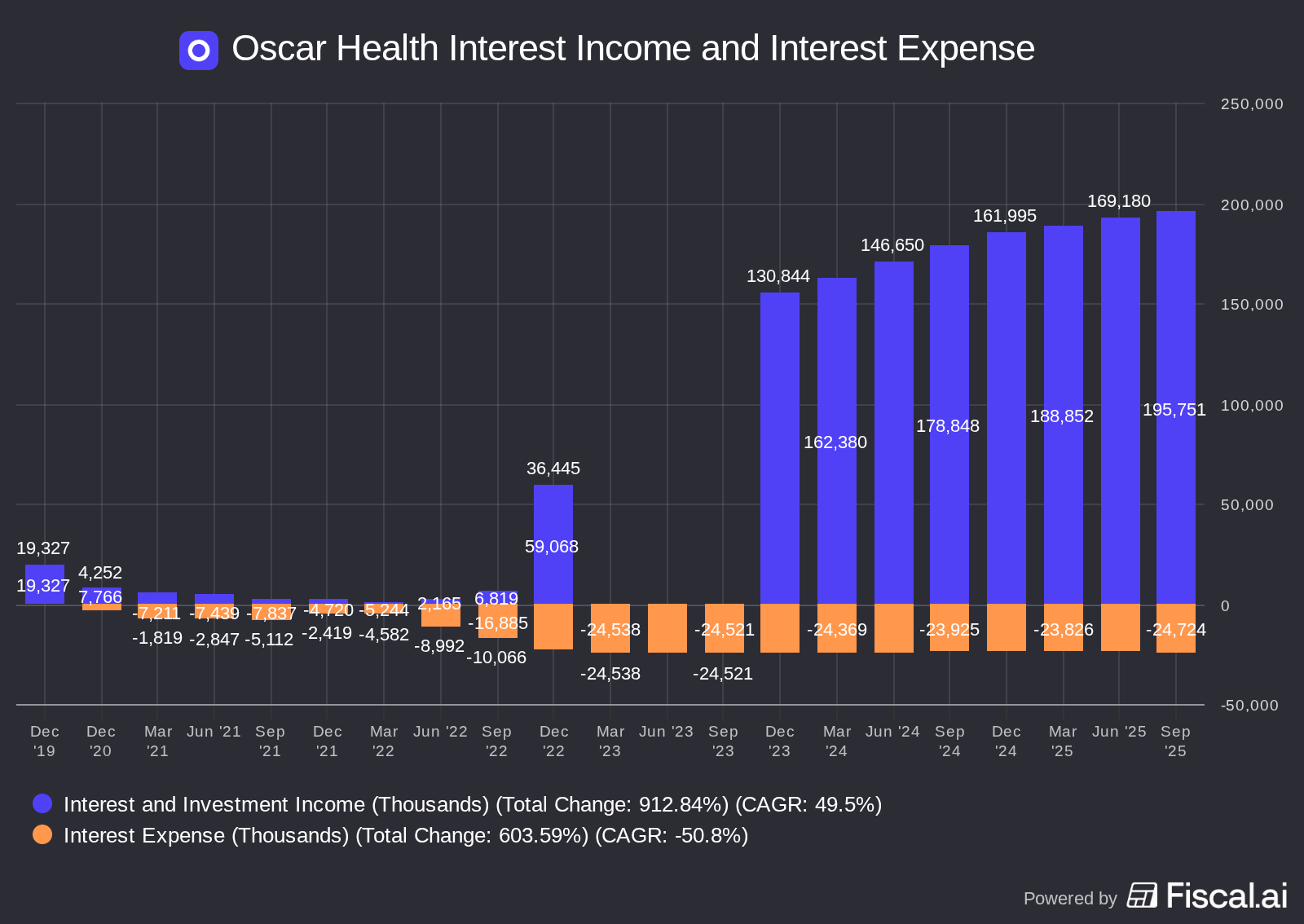

However, that overlooks net interest income, which is now well above $150 million. Assuming this falls slightly in 2026 due to lower overall interest rates, and you have Oscar Health generating an EBT (earnings before taxes) of just under $400 million in 2026.

What about five years from now? I will have no precision on these estimates. But here’s what I am confident in:

Oscar Health keeps gaining market share by expanding its geographies and stealing customers in ACA and ICHRA plans due to its better overall customer value proposition

Healthcare inflation remains above overall inflation

This should lead to a roughly doubling of Oscar Health’s premium revenue from 2026 to 2030, and that may prove conservative. Let’s say $25 billion to make it clean and easy (healthcare inflation makes this rather easy, and is our friend here).

We should also expect continued operating leverage, with the SG&A ratio now at double the premium revenue level in 2030 compared to 2026. Let’s say this results in an average operating margin of 5%, depending on the MLR for the year.

A 5% operating margin on $25 billion in premium revenue is $1.25 billion in operating earnings. Slap on some net investment income, and Oscar Health should be generating EBT of over $1.5 billion in 2030.

That is dirt cheap compared to my diluted market cap of $4.64 billion. A 20x multiple on this $1.5 billion in EBT is a $30 billion market cap. That well exceeds my return hurdle.

Managing the position

Oscar Health is currently ~5% of my long portfolio. I believe the stock has upside in 2026, with a 10x upside over the long term. There is a near-infinite runway for growth in an inflation-protected market, driven by non-discretionary consumer spending. One could even dream of a 100-bagger outcome over the next 25 years, given the stock’s current starting market cap. Baby steps. Baby steps.

Downside risks remain, sure. Every health insurer may again underprice premiums compared to utilization in 2026. Oscar Health’s customer count may collapse, and the SG&A ratio may move in the wrong direction, leading to another year of operating losses. Its counter-positioning against the incumbents could somehow evaporate if the competition gets its act together by making investments in modern technology, customer experience, and the ICHRA/ACA marketplace. Oscar Health’s history of market share gains could abruptly stop.

Except for the inherent year-to-year uncertainty around premium pricing and the MLR, these bear cases have little validity or are downright absurd to worry about, given Oscar Health’s disruptive position in the health insurance sector.

At the current stock price, Mr. Market is anticipating further pain for Oscar Health in 2026. I believe this provides us with downside protection in case something goes wrong.

I plan to purchase more Oscar Health stock in 2026. I will sell if I end up being wrong on MLR stabilization and SG&A leverage.

-Brett