Remitly Global: Is It Truly That Bad? (Ticker: RELY)

Updating after Q3 earnings. My thoughts on what will make the stock work over the next three years

Today’s newsletter discusses Remitly Global (Ticker: RELY). Before we get into the meat of things, I want to surface a recent announcement from the founder/CEO of Gambling.com Group:

When insiders are buying at the same time as you, it is a signal that you are onto something. This tweet greatly increased my conviction in Gambling.com Group stock. Here is a link to the full report if you missed it:

And now, to the main event.

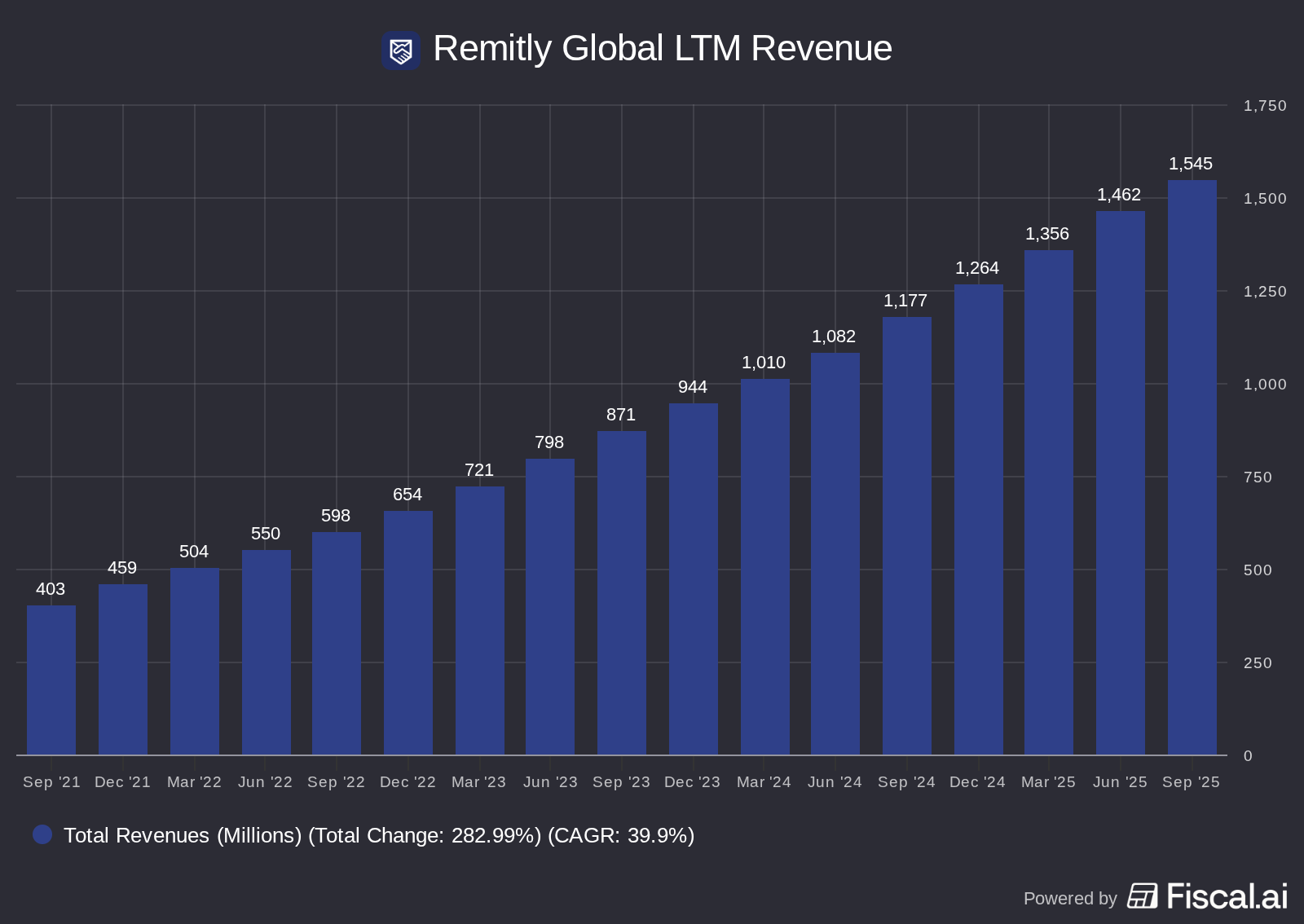

Remitly Global went public in September of 2021, selling shares at a price of $43.

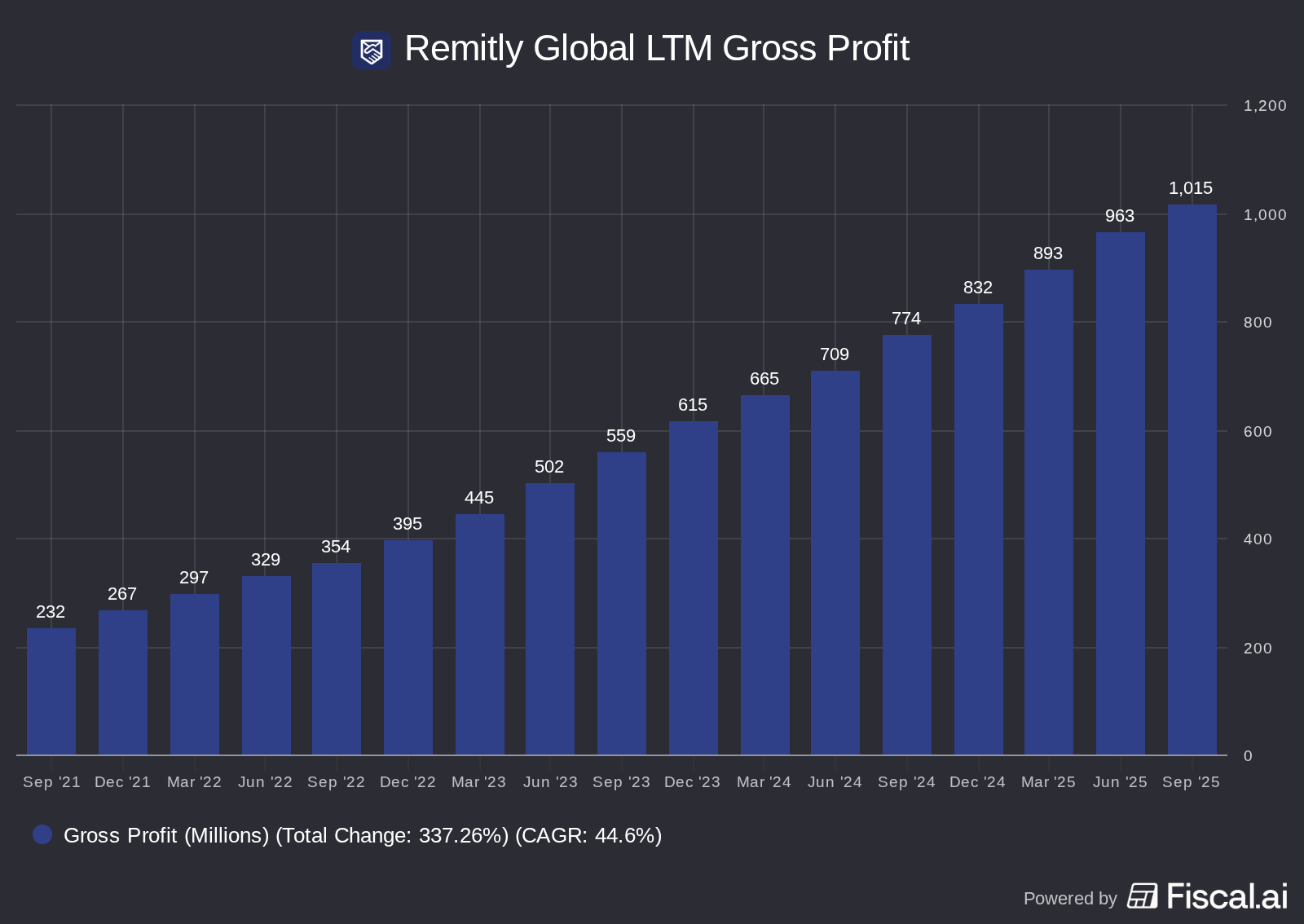

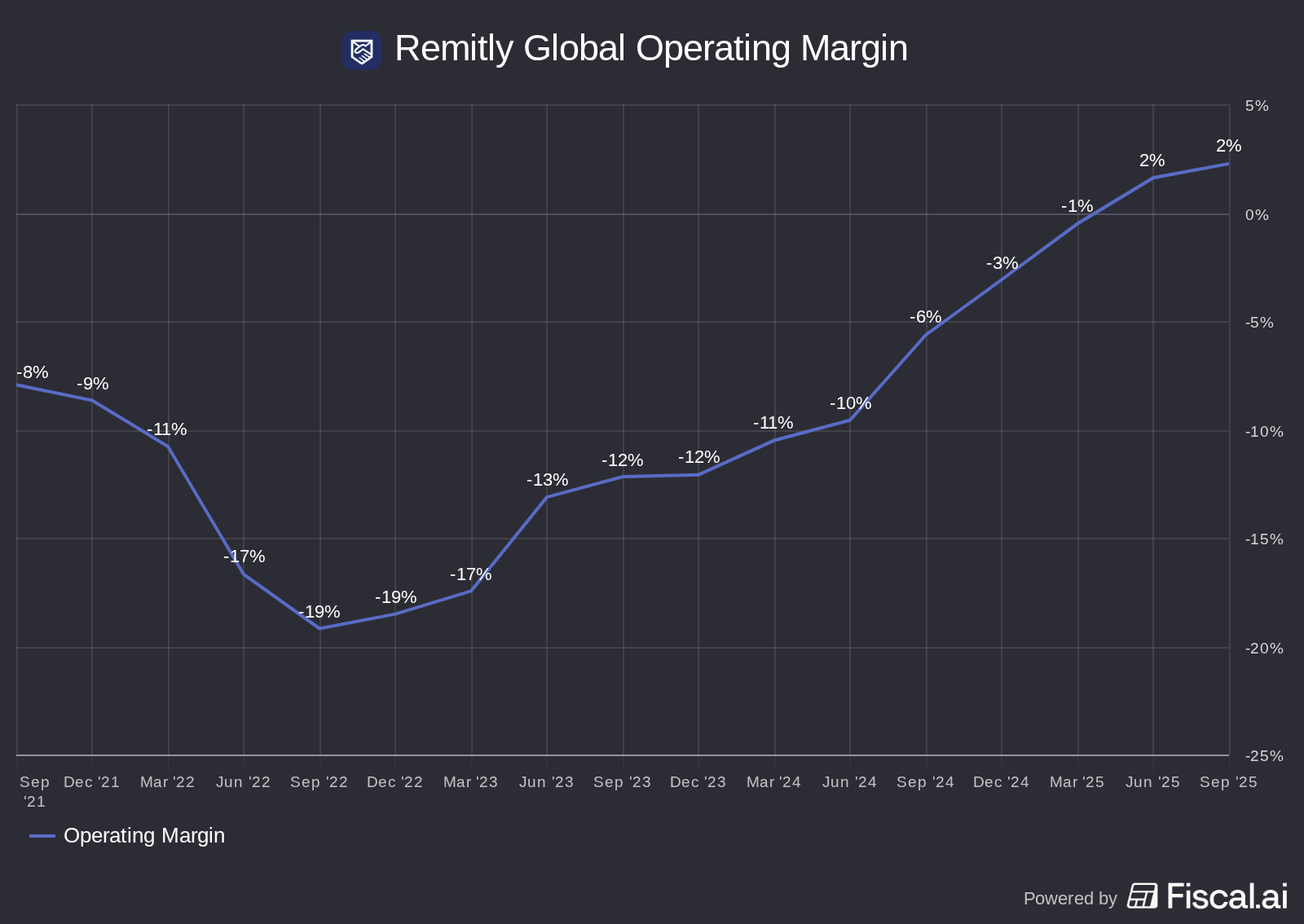

Since then, its LTM revenue is up 283%, a 40% compound annual growth rate. Gross profit is up 338% (over 44% compounded). Operating margin has flipped from negative to positive. All of its KPIs have moved in the right direction.

Its share price? Down 73% from all-time highs, to $13.08 as of this publishing on November 28th, 2025.

Investors are (again) bailing on Remitly. I cannot figure out why. The stock now trades at just 2x gross profit, the business is expected to keep growing in the double-digits, and management is starting to accelerate repurchases.

We are getting an Investor Day on December 9th. Your author will be watching diligently (and praying for speaker brevity). This newsletter is coming before the Investor Day in order to get my analysis out on the business before management spoonfeeds it to Wall Street. When a business is temporarily misunderstood – as I believe is the case with Remitly today – then an Investor Day can spark a rapid re-rating if everyone gets on board. Take a look at Adyen’s stock price chart two years ago as an example.

Here are my thoughts on Remitly’s Q3 results, valuation, and managing my position at a pivotal moment in the company’s history.

For a full introduction to Remitly’s business, I’d recommend reading my report and listening to our podcast from 2024:

Dissecting the Q3 results

Remitly reported on November 5th. The core KPIs were solid:

$19.5 billion in send volume, growing 35% YoY

8.9 million active customers, growing 21% YoY

25% revenue growth

Positive GAAP net income and positive adj. EBITDA

Send volume is outpacing revenue growth because of Remitly’s growing share of high-value senders and small business customers. These are valuable customers, but will have a reduced take rate compared to smaller dollar senders.

Over the long run, I expect Remitly’s take rate to steadily come down as it gains economies of scale across its infrastructure and operating expenses, which will at the same time steadily expand its competitive edge.

What I care about is growth in total gross profit dollars.

As the chart from the introduction illustrates, Remitly has produced consistently strong gross profit growth since going public. Last quarter was no exception.

So why did investors balk at these earnings?

Two things spring to mind: stalling marketing efficiency and early 2026 revenue guidance. Both will be examined below.

Examining Investor concerns

When having trouble identifying why a stock is down, the easiest thing to do is pose an open-ended question on Twitter. People love to tell you why you are wrong.

Multiple people responded with concerns around marketing efficiency, or lack thereof, for this business. Others were worried about the slow 2026 revenue guide.

Let’s examine these claims further.

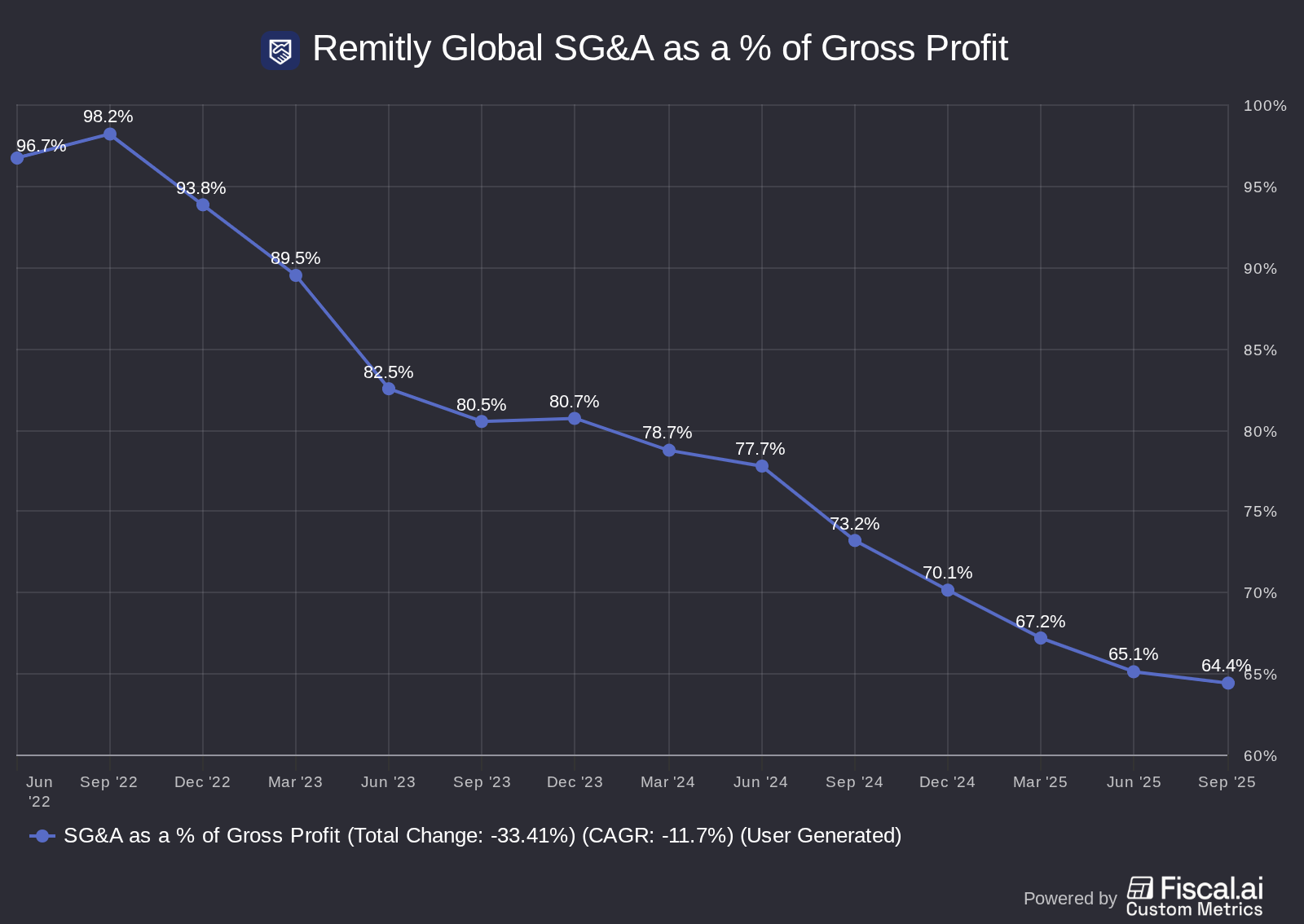

First, we can look at Remitly’s total Selling, General, and Administrative expenses as a % of gross profits. Over the last few years, the company has made progress on the operating expense line. Bringing operating expenses from 100% to 65% is fantastic leverage of the P&L, allowing Remitly to invest heavily into product development (which is not included in SG&A on Fiscal.AI) while also generating positive GAAP operating income and positive free cash flow.

However, the last two quarters have seen a slight reversal in SG&A leverage.

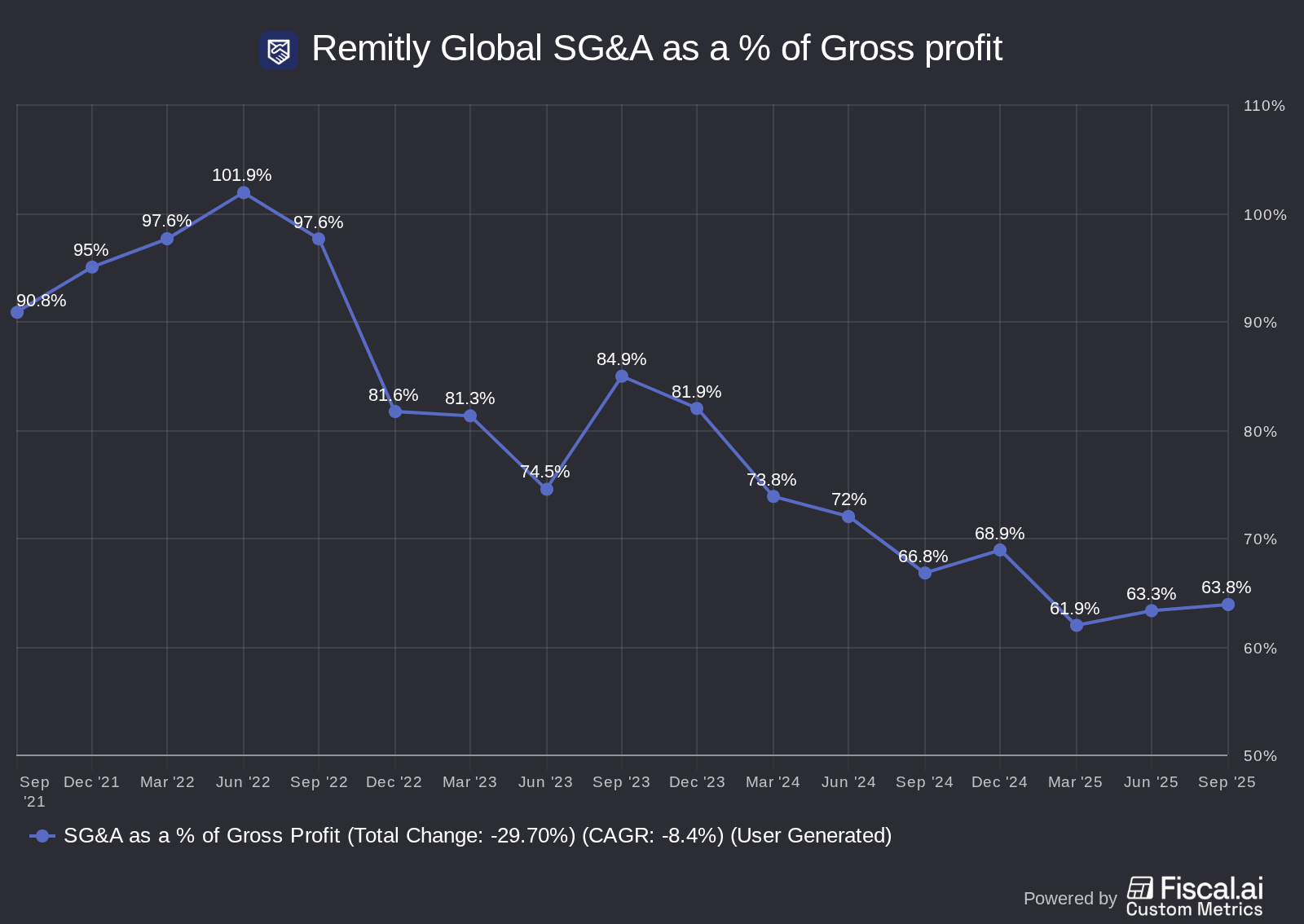

Is this what is distressing investors at the moment? Let’s take a closer look at actual marketing spend as a % of gross profit in Q3, starting in 2020:

2020: 52.0%

2021: 51.7%

2022: 43.8%

2023: 39.3%

2024: 33.8%

2025: 33.6%

Here are the full-year figures, ending with LTM ending Q3 2025:

2020: 50.2%

2021: 45.3%

2022: 43.2%

2023: 38.1%

2024: 36.5%

LTM 2025: 32.9%

From 2020 through 2024, Remitly made steady progress leveraging its marketing spend. In 2025, it looks like it is…still making progress on this trend? Let’s not kill the thesis on one quarter of slowing efficiency (a quarter with a bunch of new product launches, it should be added).

There is no reason to think Remitly has suddenly lost its marketing chops. Customers stick around with this product with definable lifetime values, and I think the stickiness will grow as send fees are lowered and new personal finance products get layered on. From 2020 to today, the company lowered marketing spend as a % of gross profit from just over 50% to just over 30%. It feels reasonable to believe there is a path to at least the low 20s by 2030.

Remitly is expecting 28% revenue growth this year. In 2026, management is initially guiding for revenue growth in the “high teens” range, which I will ballpark to 17% - 18%.

Tailwinds to revenue growth will be expanding with high-value/business senders, new product penetration, and new corridor penetration. Management was cautious in its initial guidance for 2025, likely due to the lapping of 34% revenue growth in Q1 of last year and stated uncertainties around U.S. immigration policies.

Would it be better for Remitly if this immigration crackdown weren’t occurring? Maybe. But I think any investor tied up in knots on this issue needs to look at the big picture.

Yes, revenue growth is slowing. But that is to be expected as the business gets larger. Remitly has gone from a small market share taker to one of the biggest players in the sector, and it cannot grow revenue at a 40% annual rate forever (no business can). 18% revenue growth would be just fine in my book for 2026, especially if they are facing a temporary headwind in the United States.

Speaking of which, let’s look at those deportation numbers. Has every immigrant been kicked out of the United States?

We are currently at under 20,000 deportations per month in the United States. For context, there are an estimated 50 million total immigrants in the country. Even if the border is closed forever, this pace of deportations is just a small sliver of the total remittance sending demographic. Remember too that Remitly is not just for immigrants and is diversifying away from North America.

Trump’s immigration crackdown is not going to kill Remitly. It is a company with a clear path to keep taking share of an industry that has generally grown above GDP (and is protected by inflation). Consistent market share gains, general industry tailwinds, and expanding to new financial products give me confidence that Remitly can grow its revenue in the double-digits for many years into the future.

Either way, the immigration crackdown does not concern me.

Why has operating margin expansion stopped?

Remitly’s GAAP operating margin is now positive, but has hovered around 3% for the last few quarters. Investors likely wanted more from this metric. Combine a lack of margin expansion with an expected slowdown in revenue growth next year, and, well, it isn’t surprising to see Remitly’s stock price in the gutter.

I do not believe anything is wrong with Remitly’s core business. It is not – to use one of my favorite analogies for consumer internet companies – running fast on the treadmill just to stay in place. It has predictable and durable earnings coming from its existing remittance customers.

Margins are simply not expanding as fast as investors hoped because the company has found multiple avenues for reinvestment. This is a good thing.

Remitly is beginning to expand its platform upmarket to wealthier senders and small businesses, expand geographically to new remittance corridors, and has just added a suite of new personal finance products to grow beyond foreign currency transfers.

Business penetration seems to be going well. From the Q3 call:

“The number of total businesses using the Remitly platform grew sequentially this quarter to nearly 10,000, and average transaction sizes are roughly twice those of our core consumer category.”

Businesses can be reliable high-volume senders. Take rate will be lower, but these 10,000 and growing business customers likely have similar or better returns on marketing spend vs. individuals, while expanding the company’s runway to steal market share from existing remittance players.

Geographical expansion is self-explanatory and should remain a steady slog of jumping through regulatory hoops.

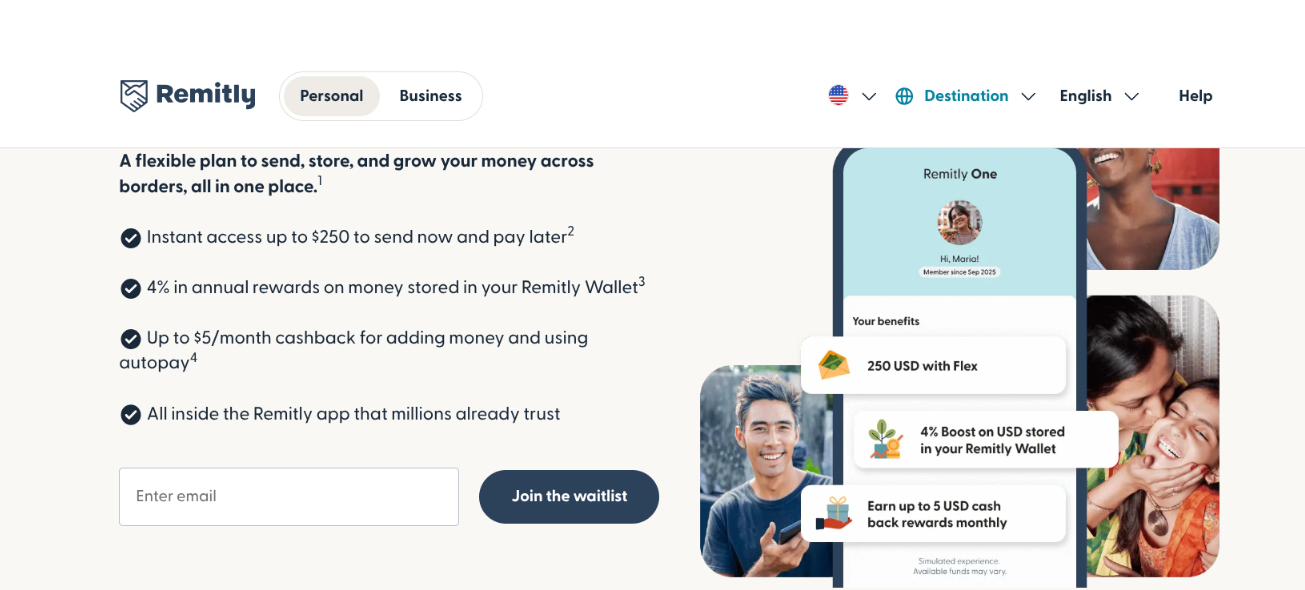

What is not self-explanatory is the launch of Remitly One, Remitly’s new subscription service that bundles its new financial services products.

Remitly One members pay $8 a month to get access to “send now, pay later”, cashback on money stored in the Remitly Wallet, and other perks. What is not mentioned in the screenshot is the development of the Remitly digital debit card. The company is focused on adding full-fledged banking services for its members, allowing them to store and spend money through the Remitly ecosystem.

There are already 100,000 Remitly Flex users (send now, pay later) who pay $8 a month to use the service. By my math, that is already $10 million in subscription ARR and 100,000 customers who are growing their relationship with Remitly. Not bad for a product that launched in September. I expect there is room to convince millions of the power remittance users to sign up for Remitly One in the coming years.

As a start-up, Remitly focused intensely on serving remittance senders from North America to India, Mexico, and the Philippines. Now, it is embarking on a journey to become a global platform for not just sending money, but also saving and spending money. It is not just going to serve small individual customers, but anyone – or organization – in need of international money transfer services.

In order to launch all these initiatives, Remitly is going to spend upfront on product development and marketing. Operating margin will be suppressed in the interim. However, if you are a believer in Remitly’s unit economics – as I am – then this company is poised to greatly expand operating margins as these new endeavors begin to scale.

Valuing Remitly stock

Again, I will reiterate my lack of detail when it comes to valuation. If you are an investor looking for detailed spreadsheet work, this newsletter is not for you.

When valuing Remitly, I am looking at two metrics: operating margin and revenue growth. That’s it. If these two metrics move in the direction I believe they will, Remitly’s stock is incredibly cheap today. Of course, a lot of factors go into revenue growth and operating margin, but at the end of the day, this is all that will matter for getting the stock up.

Given Remitly’s steady opportunity to take market share in individual remittances and the initial success of its new products, I believe it is reasonable to assume 15% annual revenue growth for this business over the next five years. A steady market share gainer is the easiest way to get comfortable projecting durably high revenue growth, and Remitly is in the sweet spot as the largest disruptor but still with under 5% share of the market.

In 2025, the company is expecting to generate $1.62 billion in revenue. Grow that by 15% annually for the next five years, and you have a business doing $3.26 billion in sales.

With the context discussed above, I believe it is also reasonable to assume Remitly’s operating margin can expand to at least 20% over the next five years, if not higher.

That would give the business $652 million in operating earnings in five years. Today, the company has a market cap of $2.8 billion, or just 4.3x these 2030 earnings projections.

To add more gasoline to the fire, Remitly has close to $500 million in cash on the balance sheet, minimal debt, and a business generating a lot of free cash flow ($205 million over the LTM). Management is beginning to repurchase its outstanding stock, and while I do not expect them to lever up and take out 25% of their outstanding shares over the next few years — which they should do — the company is in a prime spot to start reducing its shares outstanding.

Altogether, Remitly's stock looks extremely cheap today. It could even be a 10-bagger over the next five years if a more optimistic growth scenario materializes and/or significant multiple expansion occurs.

Is this still an emerging moat stock?

The last gut check for Remitly is identifying whether the company still has an emerging moat.

When looking at Remitly, I initially believed there were multiple paths to an expanding competitive advantage. First, there were the regulatory hurdles to a low-cost remittance network. It has taken Remitly a decade to build up its foreign currency platform, and it still has a long way to go to further widen this advantage vs. any upstart competitor.

Second is lowering the take rate as you gain economies of scale. Remitly continues to grow its send volumes faster than revenues, thereby making its value proposition steadily superior to any potential competitor (while also blowing any legacy solution out of the water).

Third, Remitly is expanding its product suite, which will widen the switching costs for users of multiple Remitly products. If you use Remitly to not just send money back home but store money in its Wallet (acting as a bank) and spend money with its debit card, you are not only generating more revenue for the business but are much less likely to churn.

All these emerging moat characteristics remain today, and should widen over the next five years.

We have a founder-led business with an emerging moat trading at just 4x 2030 earnings. I am very comfortable holding Remitly at 10% of my long portfolio. In fact, writing this newsletter made me want to buy some more.

Next week, I will be writing an update on Crocs.

- Brett