Rambling Thoughts Ahead Of The SpaceX IPO (Ticker: SPCX)

The end state is clear.

Today, I bring you an entirely free article for the selfish reason that I want my thoughts on SpaceX timestamped in the ether before the IPO.

So, here you go.

Rambling thoughts on SpaceX and the state of the Elon Empire.

SpaceX is planning to go public at a $1.8 trillion valuation, selling $75 billion in stock to fund orbital data centers and a ~Mars colony~. 30% of the $75 billion — $22.5 billion — is expected to come from retail investors. The cult of the empire apparently has deep pockets nowadays.

The space/connectivity business is good. Nobody should pretend it isn’t just because you don’t like Elon’s antics. Elon wants you to forget about launch costs when analyzing the Starlink segment (63% adj. EBITDA margins!), but that is not what an objective observer would do. There is no such thing as a free launch.

If SpaceX were forced to buy a Starlink launch from a third party, it would incur real costs of revenue.

Combining the Space and connectivity businesses makes sense if the goal of the space segment is to send SpaceX's internal payloads into orbit. That way, you get the true economics of the rocket launch and the services associated with it.

$15.5 billion in revenue in 2025, up from $7.4 billion in 2023. Combined EBIT/operating income of $3.8 billion. That’s it.

For round numbers, let’s say $10 billion in EBIT is well within sight over the next five to ten years. A vertically integrated rocket launch and satellite network is not cheap to build, which is why the combined capex was $8 billion last year.

$15.5 billion in revenue. $8 billion in capital expenditures. Not exactly FICO or Visa.

Capital intensity should lower your expectations on intrinsic value. A high-quality business is one that can durably generate cash that can be returned to shareholders. SpaceX is not that, and I don’t think it ever will be?

Yes, sure, it will always be cooler than FICO.

Cool does not generate excess cash flow to be redistributed to shareholders.

No matter what the tech bro media ecosystem tells you — and they will tell you their opinion on anything if it means a potentially marking up of their bags before dumping them on the public — SpaceX is not a monopoly for much longer. If we are going to value SpaceX stock on a time horizon of a one-million-person Mars colony (Musk’s goal, not mine!), then the next few years do not matter. And a few years from now, its monopoly on large payloads will have ended. If Blue Origin and Firefly continue to flop around, that’s fine; you still have Rocket Lab and its Neutron rocket coming around the bend.

I am guessing that customers like Amazon, Leo, AST SpaceMobile, or any other Starlink competitors will want to fly on other rockets, if possible, especially after SpaceX crowded out the market with its own payloads for years, creating the current bottleneck waiting to be unleashed (and making everyone mad). Starship gives them a slight leg up in size and will help them efficiently send satellites/computing racks into orbit, but in practice, it is not much larger than New Glenn or Rocket Lab.

SpaceX is a good business because of Starlink. Starlink may turn out to be a great business one day. But is it a business worth more than a few hundred billion, even if we sprinkle in some Musk pixie dust? I think not. The path to $10 billion in annual free cash flow will be treacherous.

But sure, let’s dump this onto retail at a market cap of $1.8 trillion. Lovely. I am sure this will cool the populist flames if the stock rolls over and the $22.5 billion in retail capital gets wiped out.

Space and Connectivity are not the entire business, though. Who could forget the intense negotiations between Elon Musk and Elon Musk over SpaceX's acquisition of xAI for $250 billion earlier this year?

The AI/Twitter/X business is ugly. The financial media seems to be underrating the fact that it may bring down the entire Musk empire. It is that bad. Boy who cried wolf, yeah, yeah, but this is a real turd, stop looking at it with Elon-tinted glasses.

The financials are way worse than I thought, and I have personally been replying to every Bill Ackman tweet with “@Grok, is this true?” to spitefully waste compute resources.

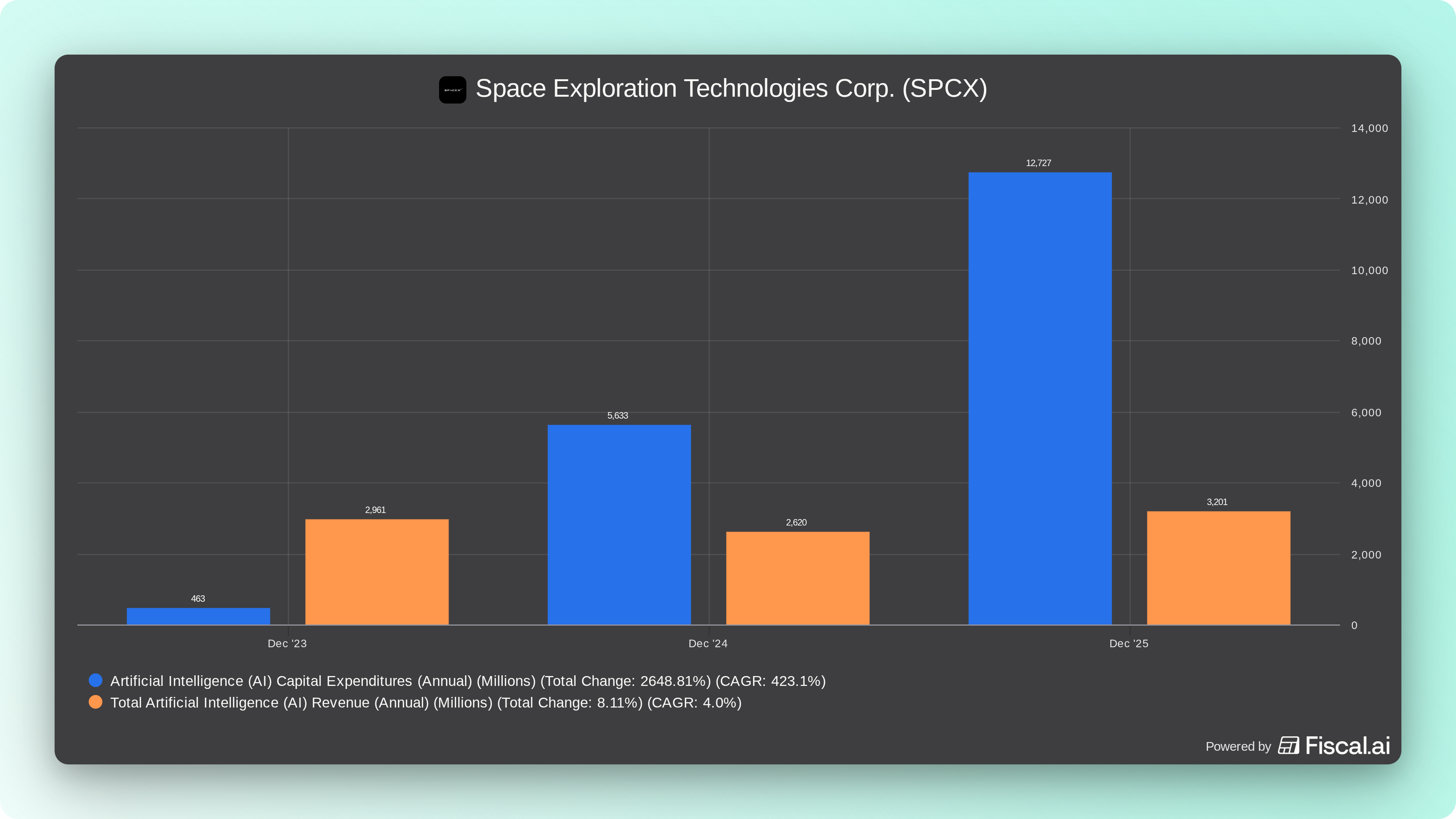

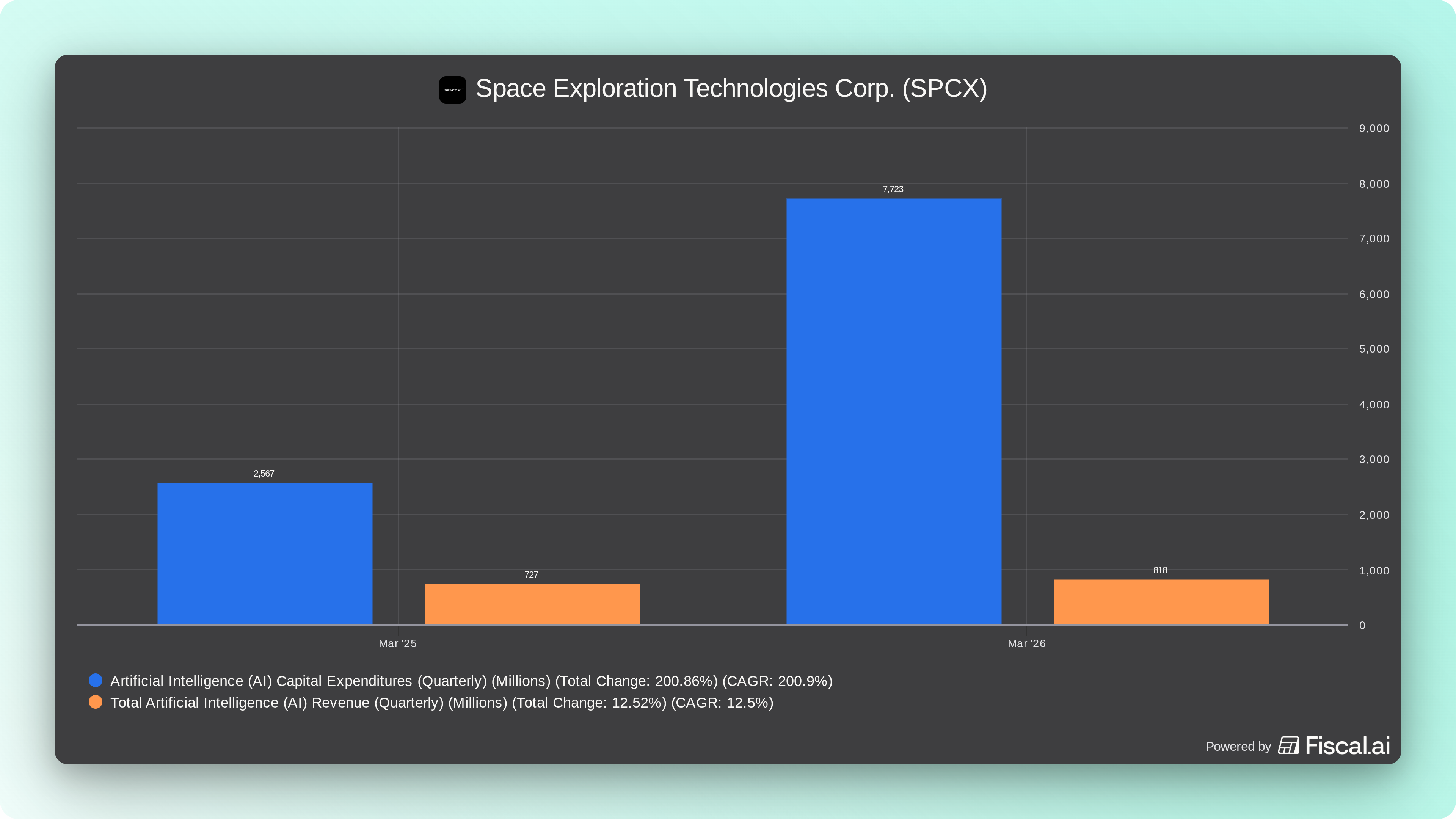

Make sure to look at these charts properly. xAI (meaning SpaceX) is a massive loser in AI. In Q1, it generated $818 million in revenue and spent $8 billion on capital expenditures just for the AI division. Some are claiming the Anthropic deal of $1.25 billion in monthly spend as a white knight, but that is a flimsy contract that can be ended whenever Anthropic wants (and they will end it and go to Google Cloud and AWS eventually).

Also, please stop and think for a minute. xAI spent a gajillion dollars to build its own data centers on Earth, yet it is already begging its direct competitors to use them. And we are now going to build these in space within the next few years, justifying a 100x P/S ratio?

The IPO isn’t even the main event. Wait, what could be bigger than this?

Everything is being set up to merge Tesla and SpaceX. We have been talking about it all year. It almost has to happen unless SpaceX can keep raising capital ($75 billion will only cover a few years of burn). We just saw the next step in this process, with “leaks” dropping to financial news outlets about “discussions” over a Tesla and SpaceX merger. I wonder who would want that narrative to start building!

CNBC notes there may be “concerns” among shareholders of the two companies regarding a merger. Either I am very confused, or this was a nice bit of humor from a financial news outlet.

I guess Neuralink is now allowing Elon to negotiate with himself. Interesting. Maybe we can add a $1 trillion valuation to that as well.

I, for one, cannot wait for the fireworks to happen. It will be $3 trillion of a mess of companies. Optimus. Cybercab. AI data centers in space. Twitter. Grok. Starship. Financial incentives for a Mars colony. Cash burn you wouldn’t believe.

My bet is to short EchoStar stock as a SpaceX proxy heading into the IPO. It is heavily indebted garbage and will likely be screwed over, as most Elon counterparties are, giving it a good risk/reward skew over the next few years.

I could not care less if SpaceX stock jumps on the day of the IPO. The next few years are going to be a slow burn as insiders dump everything on retail.

If you were to conjure up a blow-off-top for the AI bubble, you couldn’t script it any better.

Good luck to all.

-Brett

Thanks for your clear statement. It's good to see that I'm not alone in my view of the SpaceX IPO as the biggest index manipulation of all time. https://hightechinvesting.substack.com/p/spacex-ipo-how-elon-musk-is-manipulating?r=2t5wha&utm_campaign=post&utm_medium=web&showWelcomeOnShare=true