Philip Morris International: The Next Phase (Ticker: PM)

We are beginning a transition from a revenue story to an earnings and cash flow story.

“Having essentially reached our target dividend payout ratio of around 75% of adjusted diluted EPS, we have the capacity to pursue dividend growth closer to the level of earnings growth, as demonstrated by the 8.9% increase announced in September last year. Strong cash flow and EBITDA growth enable us deleveraging. We closed 2025 with an adjusted leverage ratio of 2.5x, reflecting solid progress despite the unfavorable impact of year-end currency movements on our net debt. We expect further improvements in 2026, targeting close to the 2x by year-end at prevailing exchange rates, providing increased flexibility for capital allocation. In summary, our full-year performance underscores the strength and momentum of our global smoke-free business, supported by investment in our premium brands and continued resilience of combustibles.” – Jacek Olczak, Q4 2025 Earnings Call

A great business is one that generates durable cash flow that can be freely returned to shareholders. Nothing more.

Different businesses will get you to this outcome, but the outcome is always the same. It doesn’t matter if you are invested in a small aerospace parts maker, a conglomerate of airport operators, or a multinational consumer brand. Cash flow and the return of cash flow to shareholders at a reasonable price are what we should all be hunting for.

If you understand this, you should be attracted to the nicotine sector. Cigarettes are the most profitable single product category in history. Just look at the long-term total return for Altria Group. The ability to steadily raise prices alongside durable market share and low capital intensity turned Altria Group – along with the other tobacco giants – into cash flow machines. It didn’t matter if they got an enormous fine in the 1990s or set money on fire through dumb acquisitions; shareholders still made out like bandits. Eventually, business quality wins.

Today, cigarettes are being replaced with modern forms of nicotine usage. Profit characteristics look similar, and, combined with new-user adoption, there may be multiple decades of massive cash flow ahead for the brands that win consumers’ hearts and minds.

One company has taken advantage of the nicotine transition better than any: Philip Morris International. After its acquisition of Swedish Match and the Zyn nicotine pouch business in late 2022, I became interested in following the company and realized it also held a dominant position in the heated tobacco unit (HTU) space.

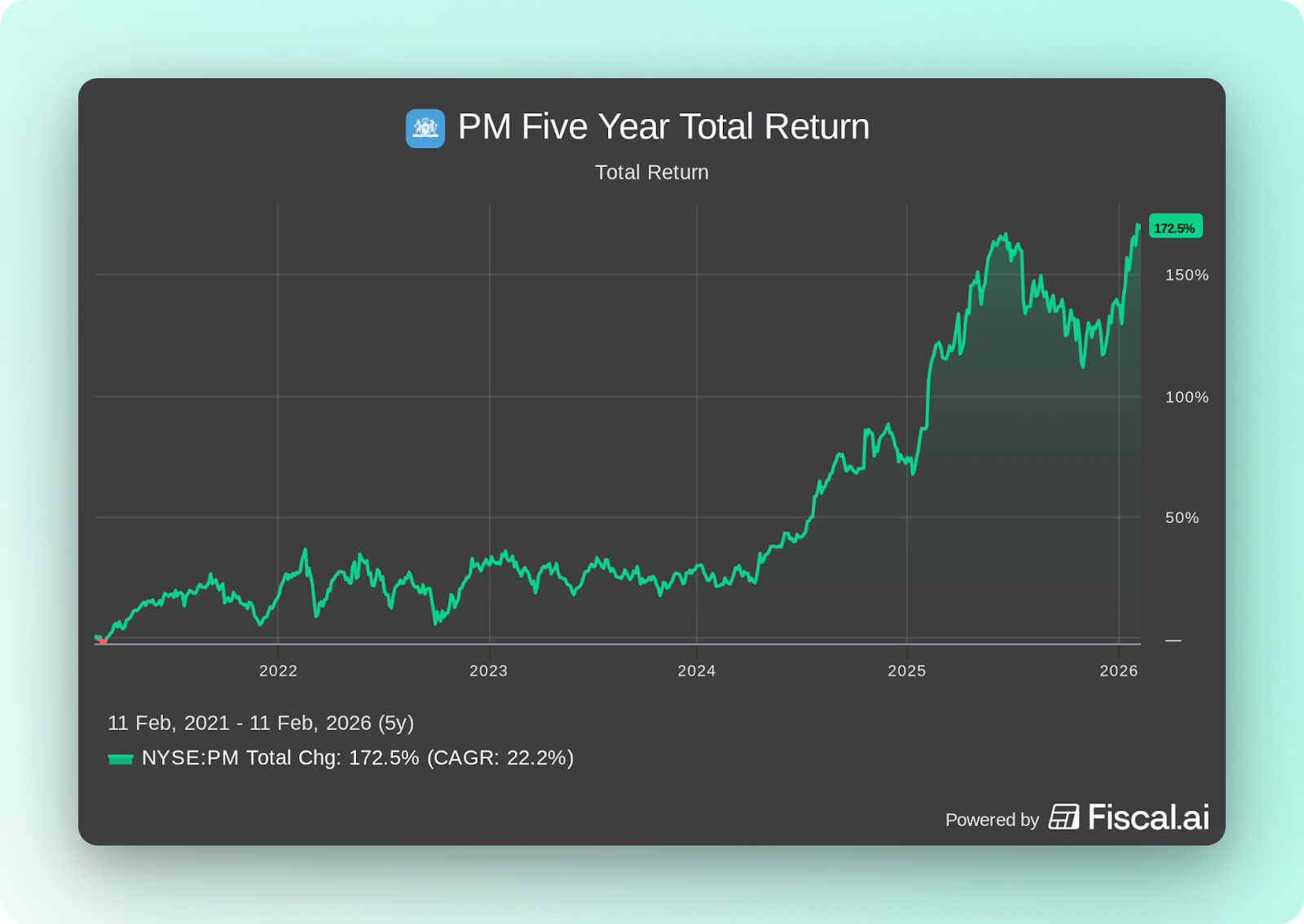

In 2023 - 2024, I purchased some shares of Philip Morris International (PM) for around $100. During the tariff tantrum in April, I decided to sell when the stock ripped to $160 while the rest of my watchlist was crashing (I used the proceeds to move into Airbnb and IBKR). As of this writing, the stock trades around $183 and has produced a total return of 171% over the last five years, most of which have come in the last two years.

The company remains of interest for Emerging Moats because of its successful transition from cigarettes to new nicotine categories, which is extending the company’s terminal value, building a new consumer branding/scale/distribution moat, and laying the groundwork for decades of durable cash generation.

In this quarterly update, I will cover:

The sustainable combustible formula

Durable HTU growth

Nicotine pouch uncertainty

Consolidated growth assumptions

Margin expansion and cash flow expectations

Dividend growth and capital returns

Is there still an emerging moat?

My investment decision

Let’s begin.

A sustainable combustibles formula

Keep reading with a 7-day free trial

Subscribe to Emerging Moats Research to keep reading this post and get 7 days of free access to the full post archives.